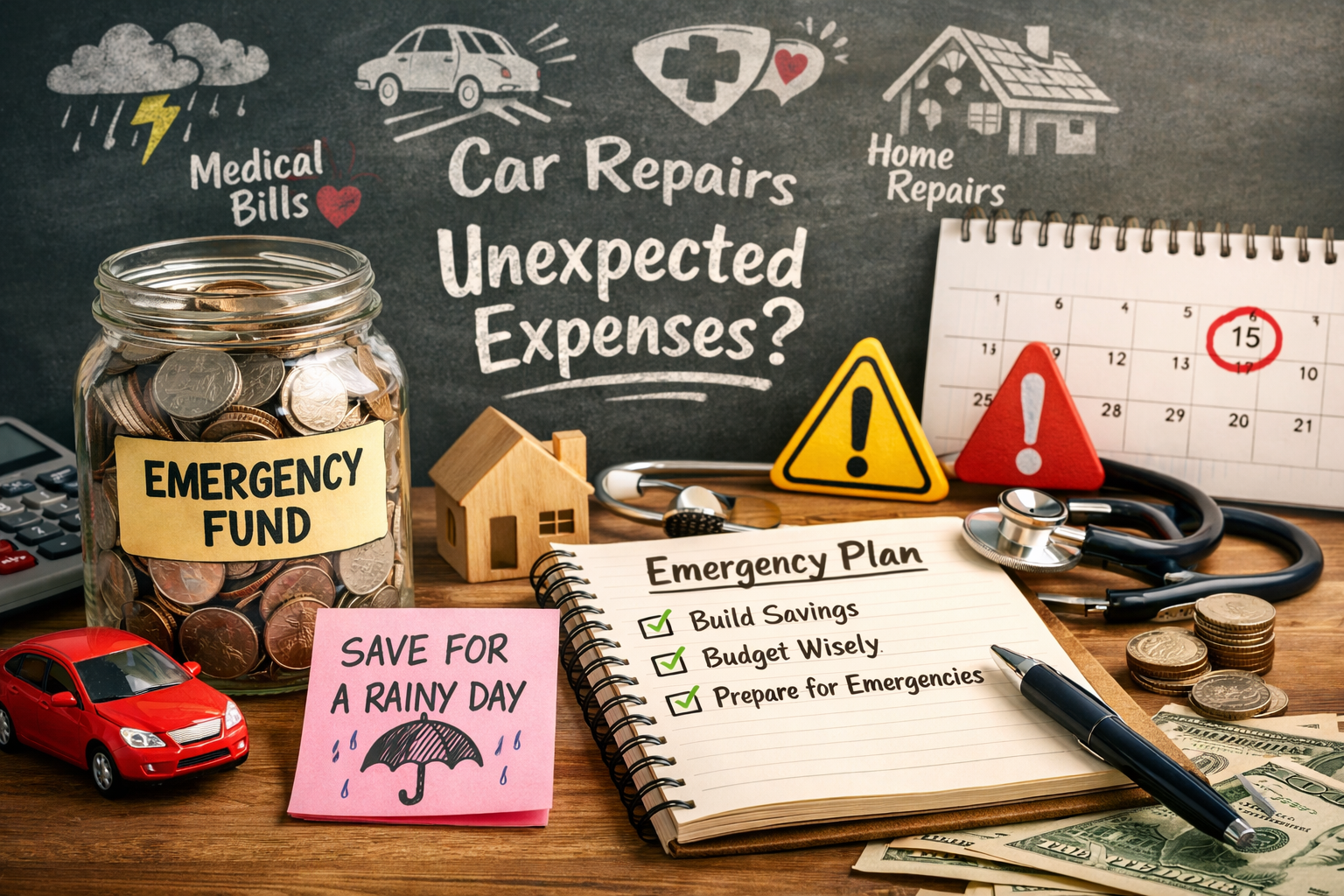

Don’t wait until it’s too late

When trying to do life as efficiently as possible, you have to be able to plan and have a sense of direction when it comes to unforeseen circumstances. Most problems in life don’t happen when you want them to, and when they finally hit the fan, you want to be able to know you are stable for an amount of time that you feel comfortable with. The amount of time you need depends on many different factors and what your threshold is.

How much is enough?

The amount that you need to save for is truly dependent on the amount that you spent on essentials on a monthly basis. This amount differs from person to person as some people have a lot more obligations and needs than others, so there is unfortunately no set number. However, the best way to get started is to just save as much as you can. Most people say you should have anywhere from 3 to 6 months worth of expenses depending on what job you are currently holding. If you have a stable job, and are able to save with not a lot of risk, then you will probably be fine with 3 months but if you have a job that you may be laid off from, or you pay a lot in rent or a mortgage, than 6 months of expenses would be a better goal to aim for. You could always strive to save for more than 3 to 6 months, but this should be a minimum and you should be comfortable to never touch this money except for a true emergencies. Don’t attempt to save all this money at once, start small, achieve little milestones, and before you know it, the power of compounding will be helping you in ways you never thought possible.

Safety of emergency funds

There is important factors to worry about when you are putting together your emergency fund that you need to think about in order to ensure that your funds are there when you need them. Most people saving in their emergency funds might be tempted to put them into individual stocks but this is extremely volatile and should be reconsidered at all costs. Stocks tend to go up and down so much, and also when you withdrawal the money you will be faced with capital gains and taxes that may wipe out a lot of your savings that you may not expect. The best place to build your emergency fund is going to be a High Yield Savings Account which on average pays you anywhere from 3% APY to 4% APY, and funds can be withdrawn within 48 hours when needed. So, not only will you be saving your money, but it will compound 3%+ every year invested, which is a lot more than cash would be doing for you in a cookie jar. Other options for emergency funds are money market accounts, but I mainly use HYSA’s.

Simple technique to achieve your goal

Achieving your goal right now might seem very intimidating but with 3 simple steps you will be able to make your goal a reality. Step 1 is going to be setting up immediate cash fund. This will be cash you will either have in your checking account or a saving account linked to it that you can access at any given time for true emergencies. Step 2 is going to be your emergency fund. This emergency fund is going to be for bigger circumstances like job loss, car repairs, or a medial expense. The emergency fund goal we are shooting for is going to be 3 to 6 months worth of your expenses per month, and it should be held in a High Yield Savings Account or a money market so you can gain some compounded interest off of your savings. Step 3 is going to be your extended safety net where you are going to hold over 6 months of your savings. This safety net fund is going to be for any type of major life change, unexpected relocations, or long term unemployment. These should be semi short term investments such as Index Funds with low fees, or treasury bills. This is a safe alternative to other savings because you will gain more interest over the long term. If you have all of these steps in place, you will have full protection for when emergencies arise which inevitably, they will. Plan now so you won’t be surprised.